The Empire of Debt

Jorge Silveira Botelho | BBVA Asset Managment

Head of the BBVA Asset Management business unit in Portugal

With more than 33 years' experience in asset management and capital markets, Jorge Silveira Botelho is responsible for promoting and managing the BBVA Group's asset management business in Portugal.

May 2026 by Jorge Silveira Botelho.

Excessive government debt has turned debt into a system of governance that sustains states and, consequently, the world order. Debt has ceased to be a mere financial instrument and has become a dangerous anchor of sovereignty.

This new paradigm, based on a changing global order, increasingly demands the understanding that capital is a scarce resource. Consequently, the greater fragmentation and the growing demand for autonomy from the regions that this new order imposes may well plunge humanity into a new era of capital-seeking.

At present, and looking beyond the enormous geopolitical uncertainty we face, there are three key issues that are closely linked to the surge in demand for capital.

The first relates to the recurring lack of control over deficits and the dynamics of debt growth in the US.

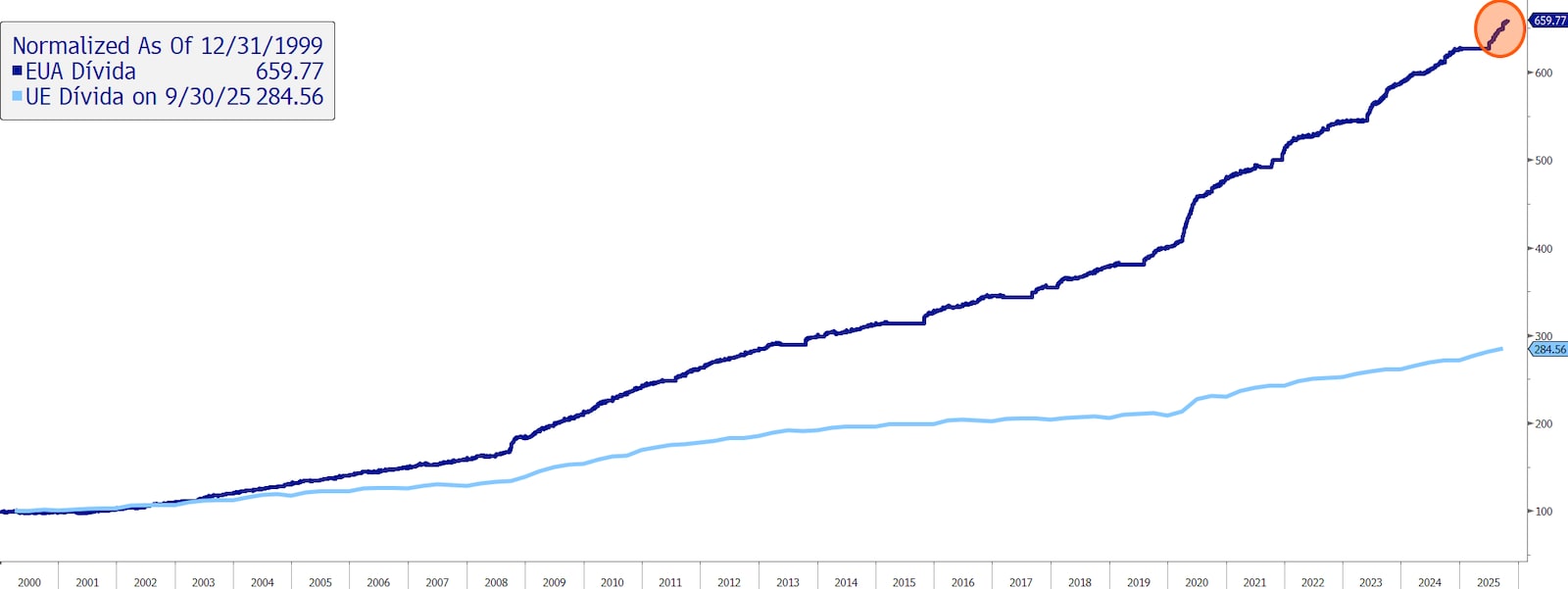

If we look back over the last 25 years, we can see that in the early 2000s, the level of US public debt, in absolute terms, rose from a figure similar to that of the European Union to more than double that amount today.

Evolution of public debt in the US and the European Union

Also noteworthy is the gradual decrease in the financing of this debt by non-residents. Between 2011 and 2025, the share of US public debt held by non-residents fell from 47% to approximately 30% (source: Treasury International Capital). It should also be noted that total public expenditure in 2025 stood at around 37.5% of GDP, with the notable fact that interest payments on the debt will already exceed the defense budget in 2025 and will account for around 3.2% of GDP in 2025 (source: Congressional Budget Office).

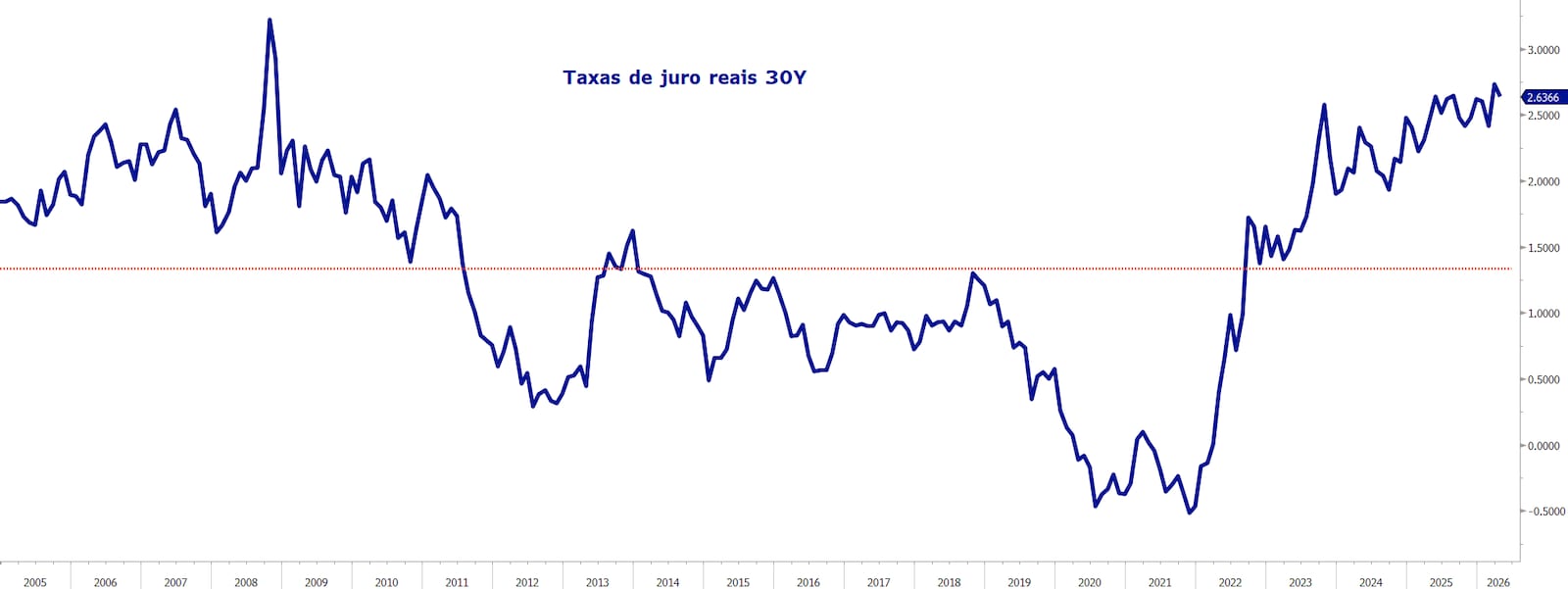

What can be inferred from this data set is that the burden of financing the U.S. economy is growing, a trend that is clearly evident in the recent rise in 30-year real interest rates in the United States.

Evolution of 30-year real interest rates in the US over the last 20 years

The second issue at the forefront of this new era of capital raising stems directly from the shift in the world order as we knew it. The urgent need for greater autonomy for both countries and regions in matters of defense, energy independence, and critical infrastructure such as transportation routes and networks will drive increased demand for capital and, consequently, its retention, whether through tighter controls on its movement or through incentives. This is already evident in countries and regions like China and some emerging countries.

In Europe, the adoption of the Savings and Investment Union, at its core, is nothing more than an effort to further develop the capital markets and create incentives to retain and transform capital. In practice, excessive state debt necessitates the development of solutions that attract savers, based on the logic of converting deposits into productive capital.

What this new autonomy for regions and countries implicitly implies is that many of the resources that were once available to other regions will simply no longer be available…

Finally, the third theme stems from the "chronicle of a death foretold" of one of the largest global sources of financing for financial assets, the famous yen carry trade. In fact, Japan is not only one of the most indebted countries in the world, with debt relative to GDP at around 250%, but

it is also one of the countries most focused on securing its autonomy in this new world order. It is true that, despite its high level of debt, more than 90% of it is held by residents (source: IMF), and Japan is also a major foreign creditor, with foreign assets accounting for about 75% of GDP. However, it is no less true that the rise in interest rates in Japan has not only reduced carry trade but is also motivating a strong movement of capital repatriation.

It follows, then, that capital will not be available in this region in the same way as it once was.

Evolution of 30-year nominal interest rates in Japan this millennium

In this context, the obvious conclusion to draw is that this new world order will usher in a new era in the search for capital, as we will witness various shifts in capital flows.

The consequences of this new reality are numerous, but one is obvious: Active management and the need for greater diversification will be two critical success factors for us to navigate this environment.

Thus, success in asset allocation will go to those who know how to navigate capital shortages, not to those who are stuck in the past.